F. Your Personal FICO Score and Your Business Credit

According to the Small Business Administration, insufficient or delayed financing is the second most common reason for business failure. Be sure your business establishes credit fast.

- Fair Isaac Corporation and your business and/or personal FICO Score

- About credit scores in general

- VantageScore

A pioneer credit score company, FICO was founded in 1956 as Fair, Isaac and Company by engineer Bill Fair and mathematician Earl Isaac.

Selling its first credit scoring system two years after the company’s creation, sales of similar systems soon followed. In 1987 FICO went public. That year also saw the introduction of the first general-purpose FICO score when BEACON debuted at Equifax.

FICO scores range from 300-850 – higher is better.

How a FICO Score breaks down (Source http://www.myfico.com/CreditEducation/WhatsInYourScore.aspx)

About credit scores

Credit bureau scores are often called “FICO scores” because most credit bureau scores used in the U.S. are produced from software developed by Fair Isaac and Company. FICO scores are provided to lenders by the major credit reporting agencies.

When you apply for credit – whether for a credit card, a car loan, or a mortgage – lenders want to know what risk they’d take by loaning money to you. FICO® scores are the credit scores most lenders use to determine your credit risk. You have three FICO based scores, one for each of the three credit bureaus: Experian, TransUnion, and Equifax. Each score is based on information the credit bureau keeps on file about you. As this information changes, your credit scores tend to change as well. Your 3 FICO scores affect both how much and what loan terms (interest rate, etc.) lenders will offer you at any given time. Taking steps to improve your FICO scores can help you qualify for better rates from lenders.

For your three FICO scores to be calculated, each of your three credit reports must contain at least one account which has been open for at least six months. In addition, each report must contain at least one account that has been updated in the past six months. This ensures that there is enough information – and enough recent information – in your report on which to base a FICO score on each report.

Credit Help Agencies Are For Profit and they have already made a deal with the banks NOT to dispute any debt if you dispute a debt they have 30 days to validate the debt.

Facts:

- Business have XX days to dispute a Credit card charge.

- Business have XX days to dispute a Debit card charge.

- Individuals have XX days to dispute a Credit card charge.

- Businesses have XX days to dispute a Debit card charge.

- 70% of all credit reports have errors.

- Old listed debt is also bad.

- Do not close credit cards.

- Do not pay off credit cards each month. 40% by card is optimal.

FICO scores have different names at each of the credit reporting agencies. All of these scores, however, are developed using the same methods by Fair Isaac, and have been rigorously tested to ensure they provide the most accurate picture of credit risk possible using credit report data.

The Fair Isaac Corporation perpetuates the mystery of its FICO scores by never releasing the details of its secret formula. Even if it were known, the fine points of its methodology are still subject to change at its discretion. In fact, FICO does not even produce the scores itself; FICO creates the software that is used by the three major credit bureaus. Those companies, Equifax, Exprerian and TransUnion, plug their own data into the FICO formula to produce proprietary results. Fortunately for consumers, FICO has disclosed a general outline of what information is used, and how it is weighted. http://www.investopedia.com/financial-edge/0212/how-is-fico-calculated.aspx or go to the source which is more intensive at http://www.myfico.com/CreditEducation/articles/

Your Payments: Your payment history is the most important factor in your FICO scores. Your history includes which of your accounts were paid on time, the amounts owed and the length of any delinquencies. Also included are any adverse public records such as bankruptcies, judgments or liens. All of this information collectively comprises 35% of a FICO score.

Your Debts: At 30%, the next most important factor are your debts. This data includes the number of accounts you owe money on, the type of debt and its total amount. Also included is the ratio of money owed to credit available, often referred to as a credit utilization rate. Interestingly, this calculation means that when a consumer opens up a new account and has more available credit, their credit utilization ratio will go down, so long as they do not incur additional debt.

Others: Beyond your payment history and your debts, the FICO formula takes into account three other factors in much smaller proportions. Your length of credit history makes up 15% of your score. This factor includes the length of time your accounts have been open and how long it has been since they have been active. This is why recent immigrants and young adults start off with lower credit scores. The types of credit used comprise another 10% of the FICO derived scores. In general, having a greater variety of differing types of accounts such as credit cards, mortgage payments and retail accounts is more beneficial than holding fewer. The last 10% of your FICO score is made up of data related to new credit applications such as the number of recent credit inquiries, and how many new accounts have been opened. Opening up too many accounts in too short of a time period is interpreted as a sign of risk and will lower your score.

The Bottom Line: When asked to sum up the entire Old Testament, the Jewish scholar Hillel is reported to have said “That which is hateful to you, do not do to your fellow. That is the whole Torah; the rest is the explanation; go and learn.” Likewise, one could summarize the FICO scoring formula by saying “You should pay your bills on time and not incur too much debt; the rest are details.” Although your payment history and the amount you owe may only make up 65% of your FICO score, it would be difficult to run afoul of the remaining criteria while paying your bills on time and carrying little debt.

There is an aura of mystery surrounding the FICO score, but it doesn’t have to be that way. While it is helpful to know the fundamentals of the FICO formula, consumers should not be tempted to feel like they can game the system. Ultimately, your FICO score will be closely dictated by your payment history and your level of debt.

Credit Reporting Agency FICO Score

Equifax BEACON® Score

Experian Experian/Fair Isaac Risk Model

TransUnion EMPIRICA®

More than one credit score

In general, when people talk about “your score”, they’re talking about your current FICO score. However, there is no one credit score used to make decisions about you. This is true because:

- Credit bureau scores are not the only scores used.

Many lenders use their own credit scores, which often will include the FICO score as well as other information about you. - FICO scores are not the only credit bureau scores.

There are other credit bureau scores, although FICO scores are by far the most commonly used. Other credit bureau scores may evaluate your credit report differently than FICO scores, and in some cases a higher score may mean more risk, not less risk as with FICO scores. - Your credit score may be different at each of the main credit reporting agencies.

The FICO score from each credit reporting agency considers only the data in your credit report at that agency. If your current scores from the credit reporting agencies are different, it’s probably because the information those agencies have on you differs. - Your FICO score changes over time.

As your data changes at the credit reporting agency, so will any new credit score based on your credit report. So your FICO score from a month ago is probably not the same score a lender would get from the credit reporting agency today.

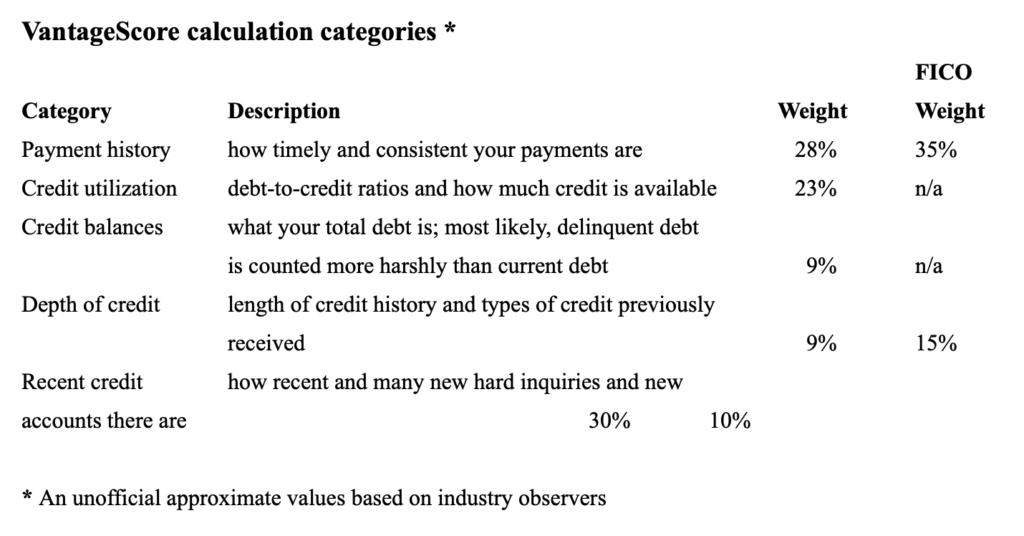

VantageScore

VantageScore is the name of a credit rating product that is offered by the three major credit bureaus (Equifax, Experian, and TransUnion). The product was unveiled by the three bureaus on 14 March 2006. The VantageScore is an attempt to compete with the FICO score produced by Fair Isaac.

Both Fair Isaac and VantageScore have allowed the public to know some information about the credit score categories and the corresponding calculation weights, but only FICO allows consumers to actually see their own score. VantageScore 3.0 does not allow consumers to know their exact score. All three agencies use the same formula to calculate the VantageScore; however, there are still discrepancies between the resulting scores if run for each of the credit reports. This is due to different data the three agencies have on the credit reports. Fair Isaac, the original creator of the FICO Score, was not involved with the creation of VantageScore’s new formula.